According to a new report by MarketsandMarkets™ – Healthcare Analytical Testing Services Market in terms of revenue was estimated to be worth $7.4 billion in 2024 and is poised to reach $12.6 billion by 2029, growing at a CAGR of 11.2% from 2024 to 2029.

The expansion of the healthcare analytical testing services market is driven by growing demand across various industries seeking quality assurance and compliance with regulations. Challenges in refining accurate analytical techniques create openings for service providers, while government efforts foster investment and creativity. These dynamics stimulate market growth worldwide, along with trends like outsourcing driven by cost considerations and advancements in pharmaceuticals. Additionally, venturing into new markets increases the demand for tailored testing, further spurring the requirement for Healthcare Analytical Testing Services.

Download an Illustrative overview: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=108923833

The Healthcare Analytical Testing Services market is diversified based on the types of services offered, encompassing cell-based assays, virology testing, biomarker testing, immunogenicity and neutralizing antibody testing, pharmacokinetic testing, and various other bio–Healthcare Analytical Testing Services. Among these, cell-based assays emerged as the dominant segment in 2023. This dominance can be attributed to the increasing utilization of cell-based assays in high-throughput screening processes. Unlike biochemical assays, cell-based assays offer the advantage of providing biologically relevant in vivo information, thereby expediting the drug discovery process. This trend underscores the growing importance of cell-based assays in meeting the demands of pharmaceutical and biotechnology companies for efficient and effective analytical testing.

The Healthcare Analytical Testing Services market caters to various end users, including pharmaceutical & biopharmaceutical companies, medical device manufacturers, forensic laboratories, hospitals and clinics, as well as cosmetics and nutraceutical companies. In 2023, pharmaceutical & biopharmaceutical companies emerged as the leading end users, holding the largest market share. This dominance is primarily due to the increasing trend among these companies to outsource their analytical testing needs. By outsourcing, pharmaceutical and biopharmaceutical firms can optimize their resources, streamline operations, and focus more on their core competencies such as research, development, and production. This strategic approach allows them to enhance efficiency, maintain regulatory compliance, and ultimately improve profit margins. As a result, the demand for Healthcare Analytical Testing Services from pharmaceutical and biopharmaceutical companies continues to grow, driving the expansion of this market segment.

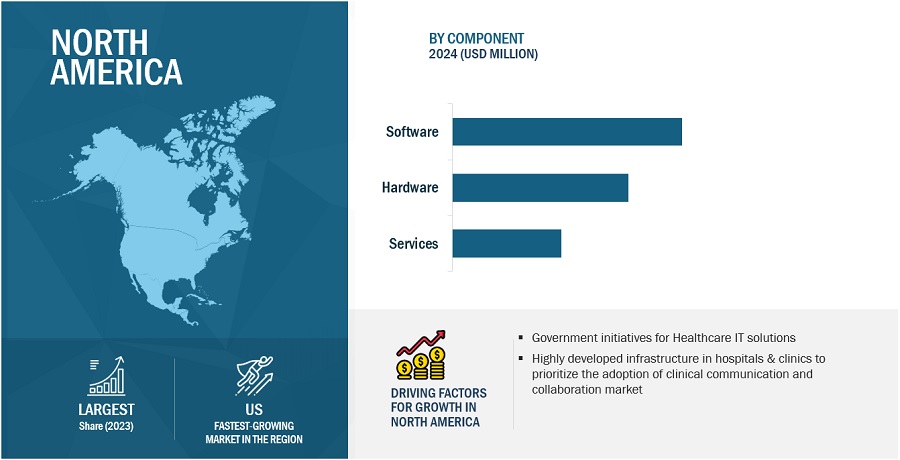

The Healthcare Analytical Testing Services market is segmented by region into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. Among these regions, North America stands out as the largest contributor to market share. This dominance is primarily driven by the burgeoning presence of biopharmaceutical and pharmaceutical companies, particularly in the United States. The US, being a hub for innovation and research in the healthcare sector, attracts significant investments and fosters the development of advanced analytical testing solutions. Furthermore, the region benefits from the presence of well-established market players with extensive expertise and infrastructure. Their robust capabilities and technological advancements contribute significantly to the growth and sophistication of the Healthcare Analytical Testing Services market in North America. Overall, the region’s favorable regulatory environment, coupled with its focus on quality assurance and compliance, further solidifies its leading position in the global market landscape.

Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=108923833

Healthcare Analytical Testing Services Market Dynamics:

Drivers:

- Changing regulatory landscape and the increasing complexity of products to drive the market

- Rising number of Clinical Trials

Restraints:

- Lack of skilled professionals

Opportunities:

- Harnessing Government Support and Technology Advancements in Healthcare analytical testing services

Challenge:

- Need for improvement to the sensitivity of analytical testing

Key Market Players of Healthcare Analytical Testing Services Industry:

The prominent players in the global Healthcare Analytical Testing Services market include Eurofins Scientific (Luxembourg), , Thermo Fisher Scientific, Inc. (US), Pace Analytical Services LLC (US), Intertek Group plc (UK), IQVIA Inc. (US), Merck KGaA (Germany), Source BioScience (UK), Almac Group (UK), Laboratory Corporation of America Holdings (US), SGS S.A. (Switzerland), Charles River Laboratories (US), WuXi AppTec Co. Ltd. (China), Element Materials Technology (UK), ICON Plc (Ireland), Frontage Laboratories, Inc. (US), STERIS Plc (US), Sartorius AG (Germany), ALS Life Science (US), Syneos Health, INC (US), Medpace Holdings, Inc. (US), LGC Limited (UK), Parexel International Corporation (US), Celerion (US). Pharmaron (China), and BioAgilytix Labs (US).

Recent Developments of Healthcare Analytical Testing Services Industry:

- In March 2024, Thermo Fisher Scientific Inc. (US), collaborated with Symphogen (US), to provide biopharmaceutical discovery and development laboratories with innovative tools and streamlined workflows for efficient characterization of complex therapeutic proteins

- In February 2024, Charles River Laboratories (US) partnered with Wheeler Bio, Inc. (US). This agreement accelerates the transition from preclinical to early clinical stages for biotech firms, streamlining processes and providing a comprehensive solution.

- In May 2023, Laboratory Corporation of America Holdings (US Collaborated with Forge Biologics (US) to advance gene therapy development and manufacturing. This collaboration aims to expedite clinical timelines, overcome analytical development barriers, and address regulatory hurdles associated with manufacturing and development processes.

- In May 2023, SGS S.A. (Switzerland), SGS SA acquired a majority stake in Nutrasource Pharmaceutical and Nutraceutical Services Inc. (Canada0), Initially acquiring 60% of Nutrasource’s shares, SGS also has the option to acquire the remaining 40% in 2026. This strategic acquisition strengthens SGS’s presence in key market segments and enhances its ability to deliver comprehensive services to clients worldwide.

- In July 2022, Eurofins Scientific (Luxembourg), acquired WESSLING (Hungary), to strengthen its presence in Central and Eastern Europe and to enhance its BioPharma Product Testing capabilities.

Research Insights: https://www.marketsandmarkets.com/ResearchInsight/healthcare-analytical-testing-services-market.asp